Does Blockchain Need Cryptocurrency? Exploring Blockchain Technology in Cryptocurrency

Untangling the Rails From the Train

In public discourse, there is a tendency to conflate blockchain technology in cryptocurrency with the coins riding on top of it. A blockchain is a tamper‑proof ledger built from blocks of data linked by cryptographic hashes; it’s like a digital supply chain record that anyone on the network can audit. By contrast, cryptocurrencies such as Bitcoin and Ether are digital tokens that ride on that ledger, providing incentives for participants to secure the network and reach consensus.

Many newcomers assume the ledger exists solely because of tokens, but blockchain concepts predate Bitcoin and have roots in distributed databases and cryptography. Because the ledger can store any structured data, from property deeds to health records, the question arises: does blockchain need cryptocurrency, or can the rails operate on their own?

This post dissects that question, explaining whether blockchain and cryptocurrencies always go together, the difference between blockchain and cryptocurrency, and other concerns that arise when people ask if a blockchain is only for crypto.

Blockchain and Cryptocurrencies: Symbiotic, Not Synonymous

To understand the relationship between blockchain and cryptocurrencies, think of a highway and the vehicles that travel on it. A public blockchain such as Bitcoin’s chain is an open‑source, decentralised ledger where each block stores transaction data and references the previous block via a hash. This chain of hashes allows anyone to verify a transaction without trusting a central authority; it functions like a public motorway maintained by its users.

Cryptocurrencies act like the toll and fuel that keep this motorway operational. They are the native economic layer that rewards miners and validators who maintain the ledger, align incentives and prevent spam or fraud. Thousands of projects now use blockchains for more than simple payments: voting systems, digital identity, food traceability, property registries and supply‑chain tracking.

For example, IBM’s Food Trust records the provenance of produce so that contamination can be traced quickly; retailers can see each step from farm to store. Enterprises also deploy permissioned blockchains where a consortium controls validation, giving each member a single source of truth across complex networks. The difference between blockchain and cryptocurrency is thus clear: the former is the distributed ledger technology, while the latter refers to the tokens that run on it.

Can Blockchain Work Without Cryptocurrency?

Short answer: yes, "can blockchain work without cryptocurrency" is more than a rhetorical question. Many businesses already operate blockchains without native coins. In a non‑tokenised, permissioned network, the ledger is maintained by a consortium of known participants who agree on the state of data. The distributed ledger provides an immutable, auditable record, while governance agreements replace the economic incentives of a public chain.

This model appeals to regulated industries: banks, supply‑chain operators and governments can benefit from shared records without exposing their data on a public network. By integrating IoT sensors and smart contracts, these networks can automate compliance checks, trace provenance and enhance operational resilience.

However, a token‑free chain isn’t a free ride. Without a cryptocurrency, there is no market‑based incentive to secure the network; consensus is enforced via legal contracts and trust in the consortium. Such systems sacrifice censorship resistance and global accessibility in favour of privacy and performance. They also require participants to finance infrastructure and security directly rather than relying on block rewards. The trade‑off lies between permissionless decentralisation and the controlled environment that enterprises often need. Many deployments accept those trade‑offs because they prioritise compliance and control over open participation.

Enterprise Use Cases: Blockchain Beyond Coins

When people ask is blockchain only for cryptocurrency, the answer is a resounding no. Real‑world implementations show that blockchains are being used to transform industries that have nothing to do with speculative tokens. Supply‑chain executives adopt permissioned blockchains to predict risk, track environmental metrics and create a single source of truth across multiple companies. Deloitte points out that a permissioned ledger allows interlinked companies to capture, validate and share data across the chain, enhancing transparency and trust without dismantling existing enterprise systems.

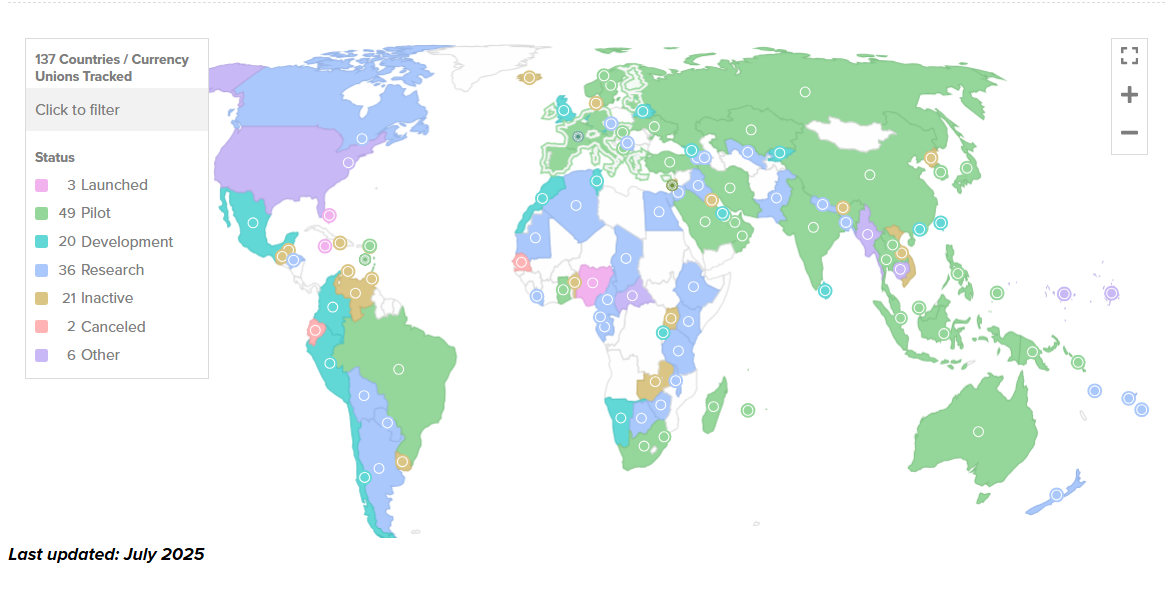

Some central banks are also exploring distributed ledgers without cryptocurrencies through central bank digital currencies (CBDCs). According to the Atlantic Council’s July 2025 tracker, 137 countries and currency unions—representing 98 % of global GDP—are exploring a CBDC, up from 35 in 2020. Although not all CBDCs run on blockchain, these experiments show that blockchains can operate under sovereign control, distributing digital cash without open‑market tokens.

It’s also worth noting that some digital-asset networks use alternative consensus mechanisms and data structures beyond traditional blockchains. IOTA’s Tangle, a Directed Acyclic Graph (DAG), enables parallel transaction validation and feeless micro-payments, while Hedera Hashgraph applies a gossip-about-gossip protocol for fast, energy-efficient consensus. Because these architectures differ from conventional sequential blockchains, some analysts describe them as distributed-ledger models that operate differently from traditional blockchains, though they remain part of the same broader blockchain and crypto ecosystem.

Hybrid Models: Tokenisation Without Volatility

Between fully public chains and closed enterprise ledgers lies a growing middle ground: tokenised assets and stablecoins. These hybrid models leverage blockchain’s programmability but use tokens designed for stability or utility rather than speculation. Deloitte observes that digital assets such as non‑fungible tokens (NFTs) enable fractional ownership of art, real estate or intellectual property, with smart contracts enforcing rights and revenue distribution. Enterprise blockchains also employ utility tokens or stablecoins to facilitate payments and incentivise participants in a controlled manner. Take Mastercard as an example:

- Stablecoin adoption is growing mainstream. Mastercard announced that it would join Paxos’ Global Dollar Network to help scale stablecoins across its network. This partnership supports regulated stablecoins like USDG, USDC, PYUSD and FIUSD, allowing them to move over Mastercard’s existing payment rails. The company notes that each wave of payment innovation gains adoption when solutions are convenient, secure and dependable. Today, Mastercard’s integrations with wallet providers such as MetaMask, Crypto.com, OKX and Kraken enable millions of users to spend stablecoins at roughly 150 million merchant locations worldwide.

- Integration with legacy payment systems. Mastercard is also expanding how its 3.5 billion cards engage with crypto, enabling merchants and gig workers to receive payouts in a stablecoin of their choice. Transactions remain protected by familiar fraud safeguards and chargeback rights, making the user experience comparable to traditional card payments.

Hybrid models like these offer a compromise: they retain the tamper‑resistant qualities of blockchain while providing the price stability and regulatory oversight that mainstream users expect. They illustrate that “do all crypto use blockchain” has a clear answer, as some tokens circulate on permissioned ledgers or payment networks rather than raw public chains.

Verdict: A Nuanced Answer

So does blockchain need cryptocurrency? Not strictly. Distributed ledgers can record transactions, votes or ownership records without issuing a native coin; permissioned blockchains and CBDCs demonstrate that viability. Yet cryptocurrencies give blockchains an economic heartbeat, aligning incentives and enabling decentralised finance.

The future will likely involve a mix of public crypto‑economic networks, private consortium chains and hybrid tokenised platforms. Understanding this balance will help stakeholders navigate the next phase of blockchain evolution.