SEC Delays Prediction-Market ETF Launches

Regulator Seeks More Details on Mechanics, Disclosures and Investor Risks

TL;DR

- The SEC delayed prediction-market ETFs expected to launch the week of May 4, 2026.

- The pause affects products from Roundhill Investments, GraniteShares and Bitwise.

- The SEC asked for more detail on pricing, disclosures, settlement risks and possible total losses.

We’ve launched the all-new COIN360 Perp DEX, built for traders who move fast!

Trade 130+ assets with up to 100× leverage, enjoy instant order placement and low-slippage swaps, and earn USDC passive yield while climbing the leaderboard. Your trades deserve more than speed — they deserve mastery.

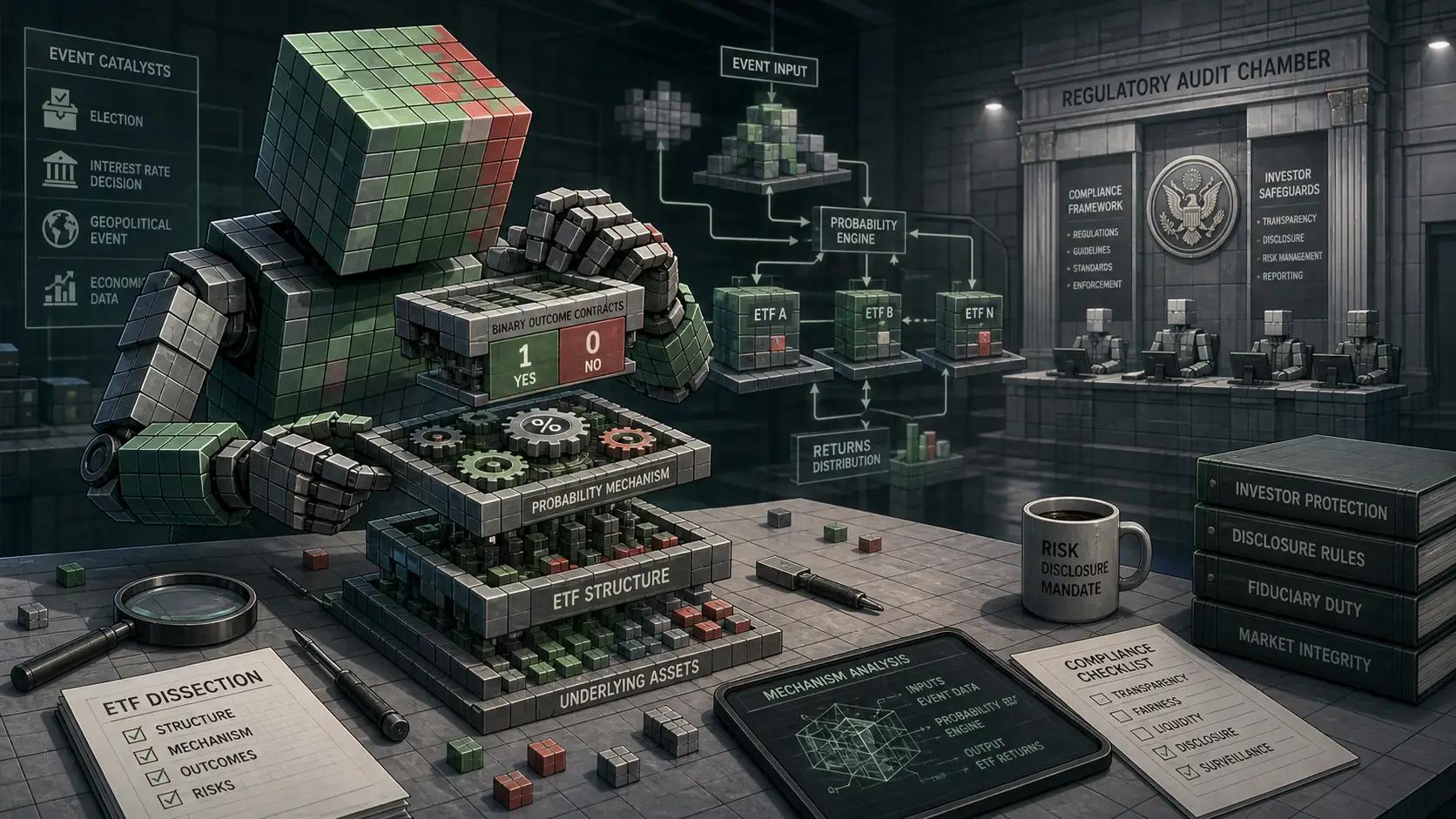

The U.S. Securities and Exchange Commission delayed the expected launch of the first exchange-traded funds linked to prediction markets after asking issuers for more information about product structure, investor disclosures, pricing mechanics and risk controls.

The information release was dated May 4, 2026, and the delay interrupted a near-term launch plan for products from Roundhill Investments, GraniteShares and Bitwise. The issuers had filed for the funds in February 2026, and the products were expected to launch during the week of May 4 after a 75-day review period.

More than two dozen proposed ETFs were affected, with one account of the filings identifying 24 ETFs from issuers including Bitwise, Roundhill and GraniteShares. The products were nearing the end of a review window that could have allowed them to become effective under ETF fast-track rules unless the SEC intervened.

SEC Questions How Prediction-Market ETFs Would Work

The SEC stepped in before the deadline passed and requested additional information on fund structure and disclosure requirements. The regulator asked Roundhill Investments, Bitwise and GraniteShares to explain how pricing algorithms would translate event-contract probabilities into ETF share prices.

The agency also asked how issuers would monitor probability changes in real time. That issue is central because the proposed ETFs would track shifting event odds rather than conventional asset prices.

The proposed ETFs would give investors exposure to event contracts tied to binary outcomes, including elections, economic data, market prices, recessions, tech-sector layoffs and other real-world events. Some proposed funds would track outcomes tied to the 2028 U.S. election, tech-sector layoffs and the likelihood of a recession.

Prediction-market ETFs would not operate like ordinary ETFs that track assets such as bitcoin or benchmarks such as the S&P 500. The products would use derivatives to track the odds of binary “yes” or “no” outcomes in event contracts traded on CFTC-regulated platforms such as Kalshi.

Event contracts normally settle at $1 if an event occurs and $0 if it does not. That payoff structure makes the proposed products more exposed to binary outcome risk than traditional asset-tracking funds.

Disclosure and Settlement Risks Move to Center Stage

The SEC questioned whether the disclosure documents adequately explain risks of total loss, settlement uncertainty and possible disagreements over event definitions or resolutions. The agency also pushed for simpler wording for ordinary investors.

The review included edge cases that could materially affect investor returns, including disputed election results and unclear event definitions. Issuers acknowledged in filings that the products carry risks including valuation uncertainty, settlement disputes and possible deviations from the stated investment objective.

Roundhill’s February filings warned that investments in event contracts involve “unique risks that differ from those associated with traditional futures, options or securities.” Roundhill also said such investments could result in significant losses, valuation uncertainty and deviations from the fund’s investment objective.

Roundhill pointed to possible settlement problems tied to how event outcomes are interpreted, including errors, ambiguities or disputes over the definition of the underlying event, the data sources used or the timing of determination. Many filings warned that investors could lose “substantially all” of their investment if the relevant outcome moves against them.

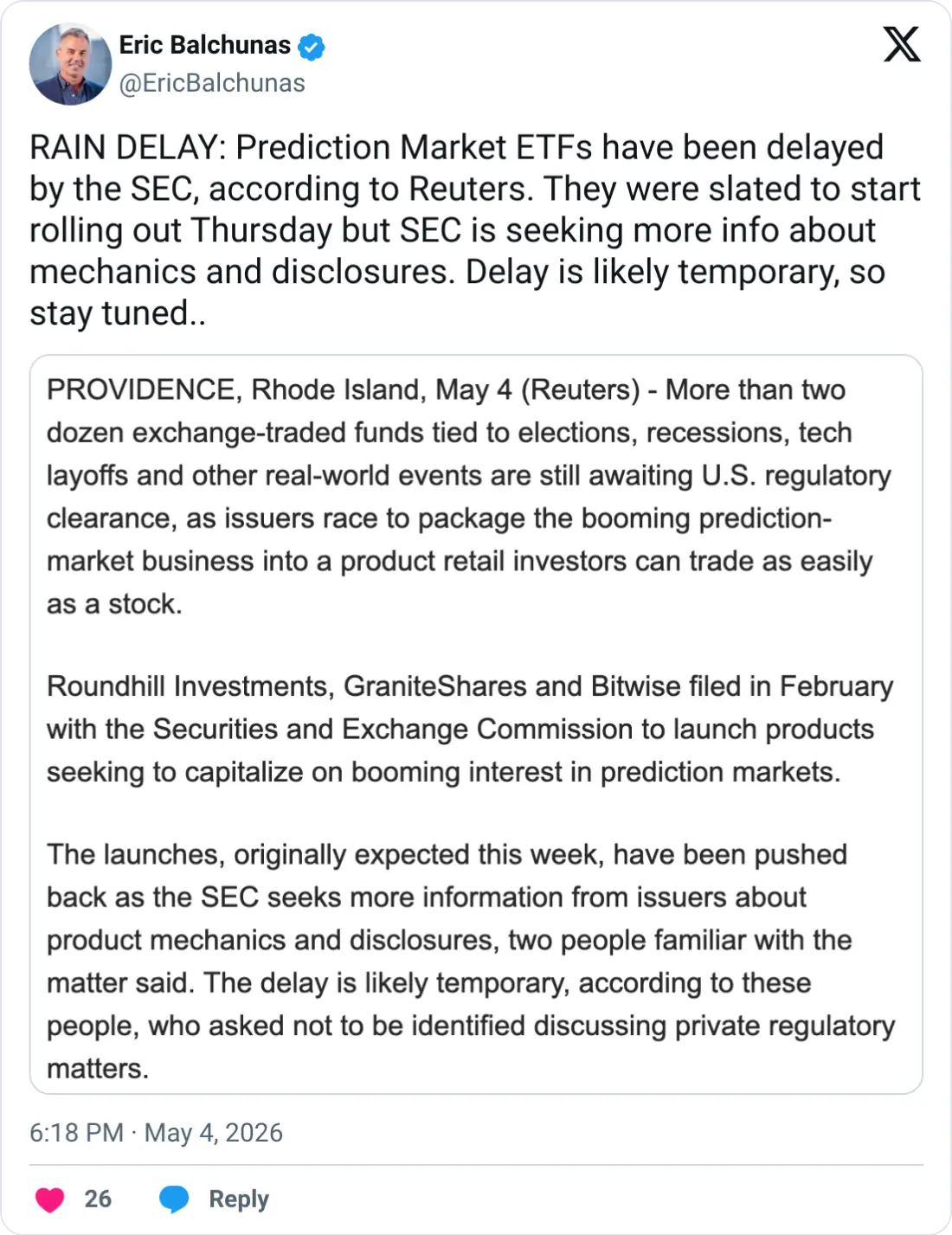

Bloomberg ETF analyst Eric Balchunas said the products were expected to start rolling out on Thursday and wrote: “RAIN DELAY: Prediction Market ETFs have been delayed by the SEC, according to Reuters. They were slated to start rolling out Thursday but SEC is seeking more info about mechanics and disclosures. Delay is likely temporary, so stay tuned.”

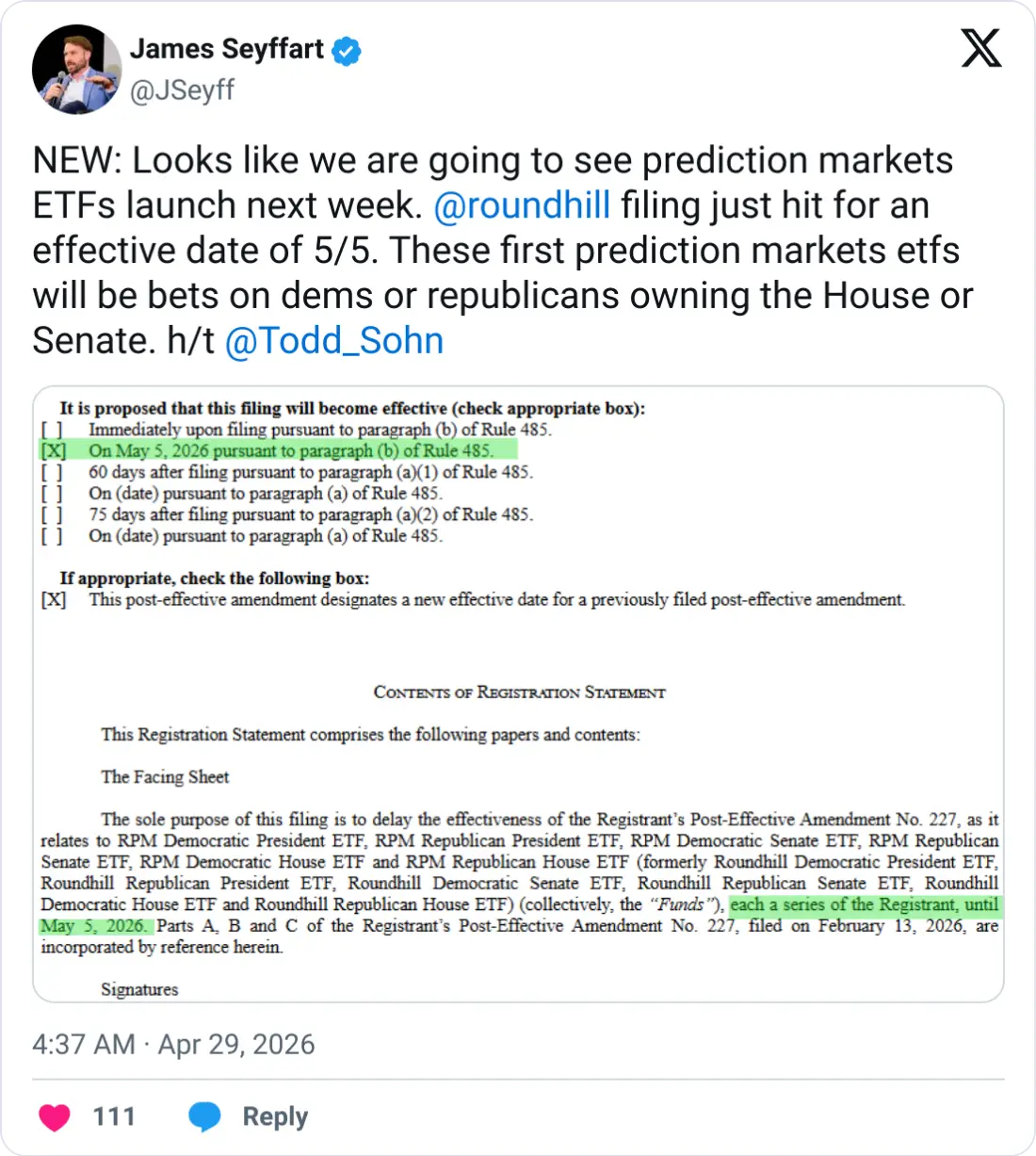

Bloomberg ETF analyst James Seyffart said Roundhill’s filing had an effective date of May 5. Seyffart said the first prediction-market ETFs were linked to event-contract outcomes such as whether Democrats or Republicans control the House or Senate.

Bitwise Chief Investment Officer Matt Hougan said regulatory monitoring typically changes alongside new financial products, comparing the current review process to earlier ETF breakthroughs such as Bitcoin funds, which required extensive regulatory scrutiny before approval. Hougan said the industry is “maturing rapidly” alongside its regulatory framework, but he would not comment on any specific timelines or outcomes.

Broader Prediction-Market Fight Remains Unresolved

The delay comes as the broader U.S. regulatory fight over prediction markets remains unsettled. The core question is whether event contracts should be treated mainly as federally regulated derivatives or as gambling-like products subject to state restrictions.

The Commodity Futures Trading Commission sued multiple states last month, arguing that event contracts fall under its “exclusive jurisdiction.” State officials pushed back against that position, arguing that the offerings amount to unlicensed gambling.

Venture firm a16z argued in favor of the CFTC on Friday, warning that a patchwork of state-level restrictions could “severely circumscribe” liquidity and limit user access.

Lawmakers are also focusing on insider-trading risks in prediction markets, especially the possibility that people with nonpublic information could place bets on political or real-world outcomes. The Senate moved last week to bar members from trading on prediction markets, citing concerns that nonpublic information could be used to place bets.

Policymakers raised concerns that putting prediction markets into ETF structures could increase speculative activity around sensitive real-world events such as elections and international wars. Lawmakers have previously examined prediction markets for potential risks tied to insider trading, market manipulation and incentives linked to significant events.

Prediction-market platforms have scaled quickly. Polymarket and Kalshi recorded a combined $85 billion in volume during the first four months of 2026, including $24.3 billion in March 2026.

For now, the SEC has not publicly issued approval or rejection decisions on the affected products. Staff and issuers are still debating structure and transparency issues, and the delay has been described as likely temporary if the SEC receives and reviews additional details from issuers.

FAQ

What did the SEC delay?

The expected launch of prediction-market ETFs from Roundhill Investments, GraniteShares and Bitwise.

Why did the SEC intervene?

The SEC sought more information on mechanics, disclosures, pricing, risk controls and settlement uncertainty.

Were the ETFs rejected?

No public approval or rejection decision has been issued.

What risks did filings describe?

Valuation uncertainty, settlement disputes, significant losses and possible deviations from fund objectives.

This article has been refined and enhanced by ChatGPT.