Vitalik Buterin’s Trustless Gas Futures Proposal Sparks Market Structure Debate Across Ethereum Ecosystem

Researchers, Builders, and Core Contributors Confront the Economics Behind a Potential Onchain Gas Hedging System

TL;DR

- Vitalik Buterin proposes a trustless onchain gas futures market to hedge Ethereum fees.

- Researchers warn the model lacks a natural short side and may fail to scale.

- Debate intensifies as Ethereum upgrades reshape throughput, fees, and protocol economics.

We’ve just launched the all-new COIN360 Perp DEX, built for traders who move fast!

Trade 130+ assets with up to 100× leverage, enjoy instant order placement and low-slippage swaps, and earn USDC passive yield while climbing the leaderboard. Your trades deserve more than speed — they deserve mastery.

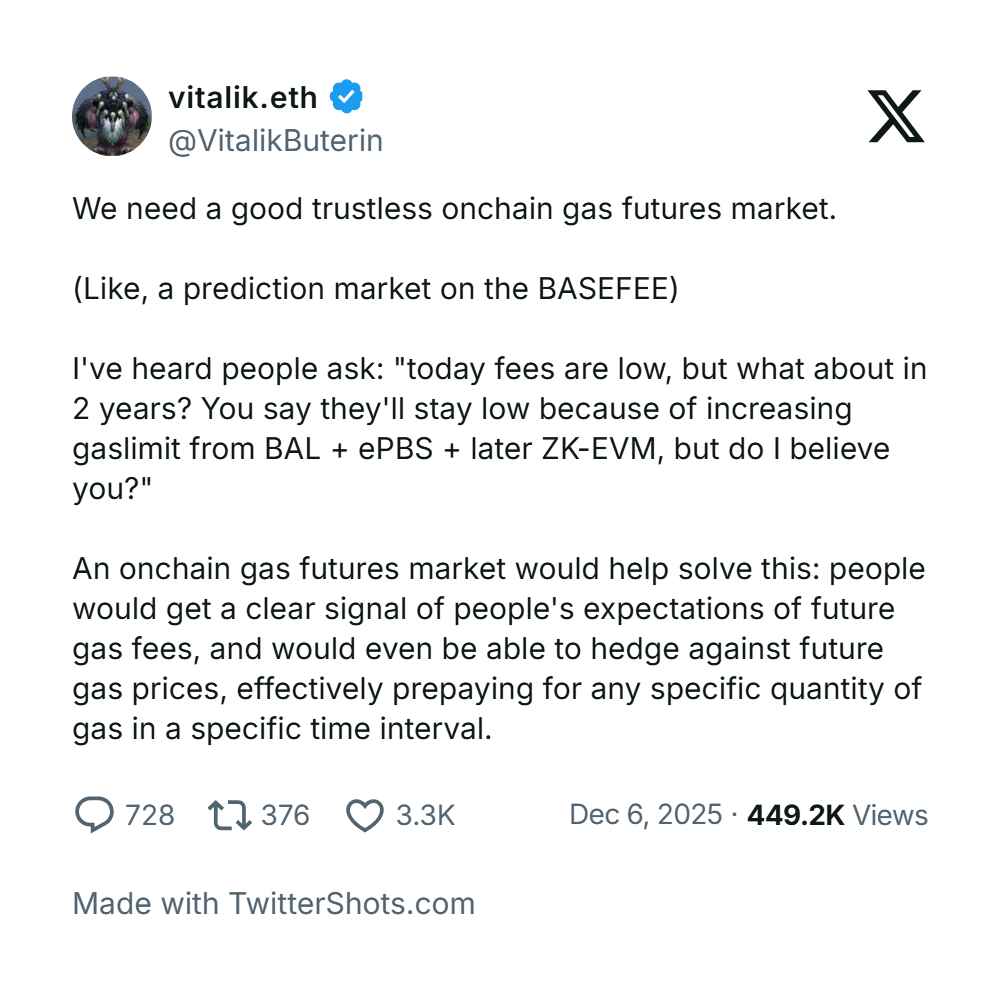

Ethereum co-founder Vitalik Buterin has ignited a new round of debate over fee markets after proposing a trustless onchain gas futures system designed to give users and developers a way to hedge against transaction costs. His idea surfaced in an X post where he said the recurring question he hears is whether today’s relatively low fees can be expected to continue over the next two years as Ethereum’s roadmap pushes scaling forward.

Gas represents the computational cost tied to any onchain action, from simple transfers to complex smart contracts. Historically, gas markets behaved like a volatility machine, swinging from manageable levels to sudden spikes during NFT run-ups, DeFi surges, or high-profile token launches. The past year has brought a noticeable reduction in these shocks as upgrades improved capacity and reduced congestion, but longer-term uncertainty still lingers for builders planning multi-year product operations.

Buterin framed the futures idea as “a prediction market on the basefee,” one that could signal expectations of future gas levels and let participants lock in pricing by pre-purchasing specific quantities of gas for defined time intervals. He argued such a mechanism would give users clarity and allow both individuals and application developers to hedge fee risk by shifting from an inherently short position on gas to something closer to neutral.

Skepticism surfaced quickly, led by Hasu, the strategy steward at Flashbots and advisor to Lido and Steakhouse. He said the concept lacks the most fundamental ingredient of a functioning derivatives market: a natural short side. According to him, many market participants are effectively short gas because they consume it and want protection from rising costs, but almost no one is structurally long gas. Without organic short sellers, he warned, any futures market would likely be thin, illiquid, and unable to operate at meaningful scale.

Buterin responded by asking whether “the protocol should be the short side,” suggesting an onchain auction model that sells rights to claim basefee revenue for at least 1 million gas per block. The idea attempts to shift part of Ethereum’s structural position—where the protocol is naturally long gas—toward neutrality by selling a predetermined portion of that exposure in advance. Yet Hasu pushed back again, saying anyone buying the basefee would effectively pay nearly all of its value to the protocol, and the only logical buyers would be those expecting prices to rise. That dynamic, he argued, creates a built-in reluctance to short because the incentive structure remains misaligned.

Martin Koppelmann, co-founder of Gnosis, added another layer of complexity by pointing to Ethereum’s burn mechanism. The burn permanently destroys a portion of transaction fees, which he said reduces the number of natural sellers who could take the opposite side of a futures contract. Validators, who otherwise might have filled that role, no longer receive the full economic benefit since the burn removes part of their upside. Koppelmann said this forces potential sellers to assume additional risk, making any hedge significantly more expensive.

The discussion arrives at a moment when Ethereum’s economic design, throughput, and fee structure are undergoing rapid transformation. The network finalized its Fusaka upgrade last week, launching a new twice-a-year hard-fork cadence and benefiting from a recent increase in the block gas limit to 60 million, which pushed throughput to record highs. Alongside these system-level enhancements, Buterin has laid out Kohaku, a privacy-focused framework meant to strengthen confidentiality across the ecosystem, and has spoken about how scaling and maturing DeFi rails have finally made “DeFi as a form of savings” viable.

Whether a trustless gas futures market becomes a workable extension of Ethereum’s economic stack remains unresolved. The debate illustrates the tension between engineering ambition and market microstructure reality, especially when protocol-level incentives and fee mechanics blur the line between what is theoretically elegant and what is financially sustainable.

This article has been refined and enhanced by ChatGPT.