Coin360 Weekly Dispatch | Crypto Market Updates & Highlights | January 11 - 17, 2026

Trade Like You Mean It: The COIN360 Perp DEX Is Live

We’ve launched the all-new COIN360 Perp DEX, built for traders who move fast!

Trade 130+ assets with up to 100× leverage, enjoy instant order placement and low-slippage swaps, and earn USDC passive yield while climbing the leaderboard. Your trades deserve more than speed — they deserve mastery.

Weekly Crypto Market Performance Overview

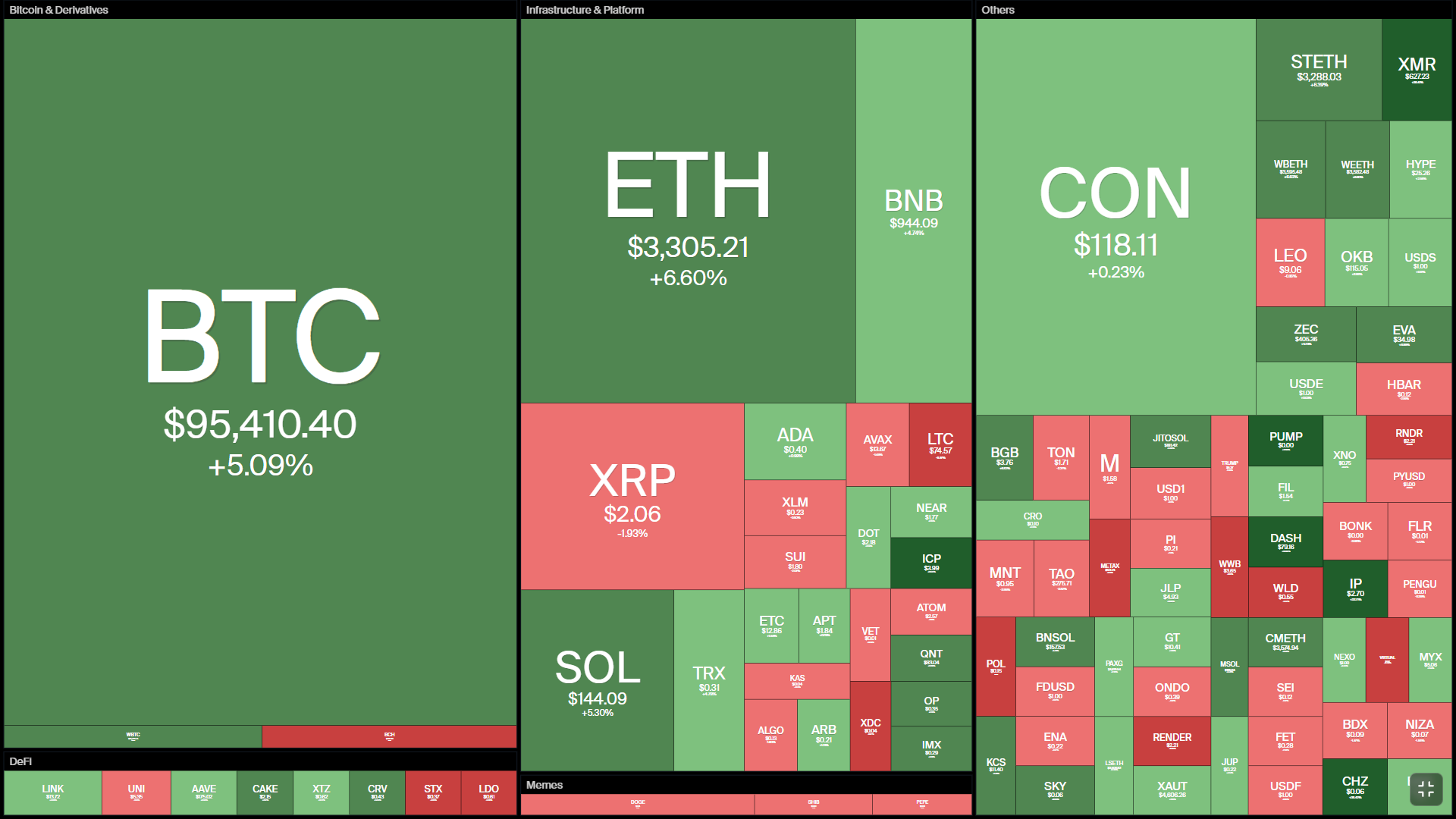

Total crypto market cap: $3.19T

Crypto Fear & Greed Index: 50 (Neutral)

BTC.D: 59.61%

Bitcoin and Ethereum posted strong weekly gains from Jan 11–17, 2026, outperforming equities in a generally mixed risk environment. BTC rose 5.09% on the week, trading from roughly $90.9K to $95.2K, while ETH gained 6.6%, moving from about $3.12K to $3.30K. Price action was constructive but uneven, with both assets setting weekly lows early in the week (Jan 12) before accelerating into midweek highs; BTC briefly reached $97.8K on Jan 14, marking the key upside inflection.

From a market-structure perspective, upside momentum was amplified by positioning dynamics rather than purely organic demand. A sharp midweek rally coincided with nearly $700M in crypto short liquidations, including roughly $380M in BTC shorts, indicating forced buying as prices pushed through technical resistance.

Fundamentally, US spot ETFs were the dominant internal driver: BTC ETFs recorded approximately $1.42B in net weekly inflows, while ETH ETFs added about $479M, with the largest inflows concentrated on Jan 13–14. At the same time, some indicators pointed to contracting stablecoin liquidity, suggesting that while price rose, underlying on-chain liquidity expansion was not clearly supportive; attribution between sustained spot demand and short-covering therefore remains mixed.

Macro conditions provided the backdrop but not a single clean catalyst. US CPI data released during the week reinforced rate-cut expectations, while political pressure and investigations surrounding the Federal Reserve raised questions about central-bank independence, contributing to dollar softness and heightened policy sensitivity. In this context, crypto outperformed traditional risk assets: over the same window, the S&P 500 fell ~0.4% and the Nasdaq ~0.7%, while gold rose ~2.1%.

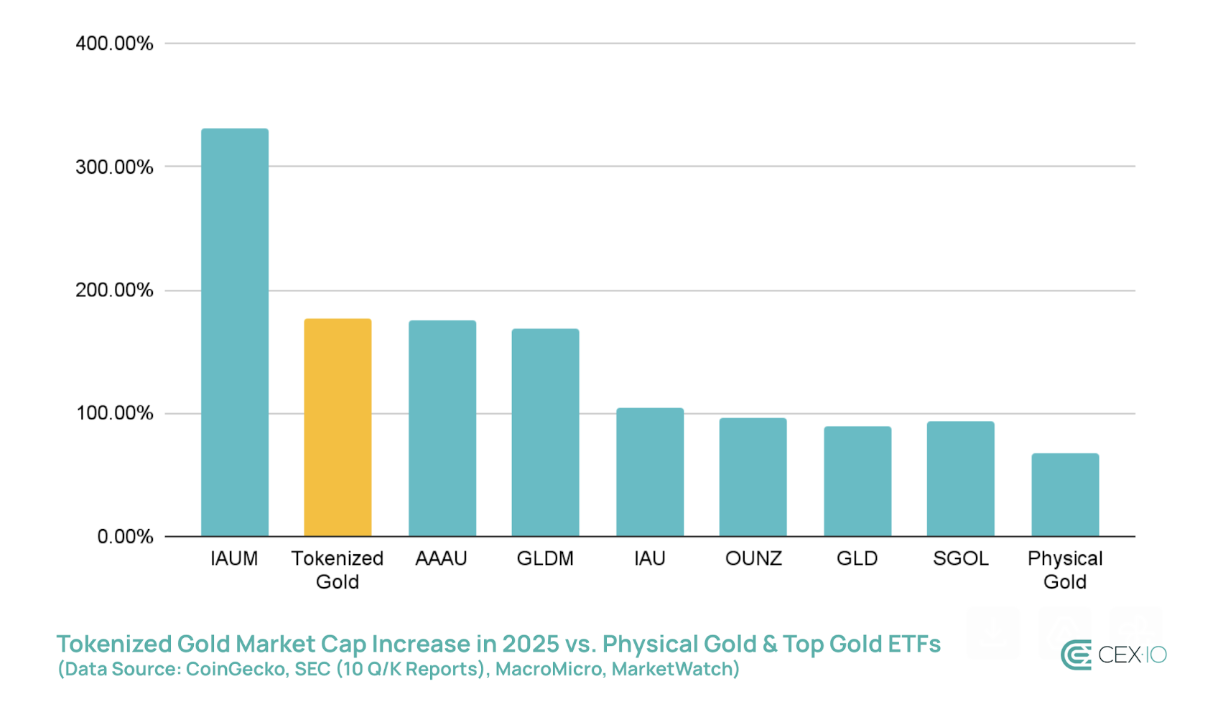

Gold and Bitcoin as Complementary Macro Hedges

Gold and Bitcoin increasingly appear as complementary macro hedges rather than substitutes. Historical analysis from Bitwise shows gold consistently dampened portfolio drawdowns during stress periods—posting modest gains or limited losses in 2018, 2020, and 2022—while Bitcoin absorbed far deeper declines but delivered outsized recoveries, including a 775% surge after 2020. Portfolios combining both assets achieved a higher Sharpe ratio (0.679) than traditional 60/40 allocations, highlighting improved risk-adjusted performance, even if volatility remained elevated.

This backdrop matters as gold-linked RWAs now account for 25% of RWA growth as per a CEX.IO report, with tokenized gold trading volumes surpassing gold ETFs, signaling structural demand beyond speculation.

Macro pressures reinforce the case: expectations of continued US dollar weakness in 2026, driven by yield erosion and external deficits, align with Ray Dalio’s framework advocating a gold–Bitcoin allocation as a hedge against currency debasement.

Policy gridlock meets “regulated crypto” reality

The week opened with U.S. market-structure momentum stalling: the Senate Banking Committee postponed its planned markup of the Digital Asset Market Clarity Act indefinitely after more than 130 amendments piled up and Coinbase warned it would withdraw support. Objections surfaced on multiple fronts—developer liability for noncustodial software, stablecoin rewards, and concerns about expanded surveillance powers—with Senate Judiciary leadership also objecting to the Blockchain Regulatory Certainty Act being folded in without consultation.

While U.S. legislation bogged down, Europe and Eurasia showed a different pattern: regulated access pathways expanding—just tightly controlled. DZ Bank confirmed it secured MiCA authorization from BaFin, positioning “meinKrypto” to deliver retail crypto trading via Germany’s cooperative banks once individual institutions complete their own notifications. Belarus, meanwhile, signed Decree No. 19 to formalize “cryptobanks” under state banking oversight, tying crypto services to licensed institutions, High-Tech Park status, and central bank supervision.

Big institutions keep building the rails (quietly, compliantly)

Against that policy backdrop, Standard Chartered’s move sat squarely in the “institutions want exposure, but with compliant architecture” lane. The bank is preparing a crypto prime brokerage inside SC Ventures—early planning, no launch date disclosed—aimed at bundling custody, financing, and market access while managing Basel III capital constraints (including risk weightings cited as high as 1,250% for certain unlicensed crypto exposures). Existing SC Ventures-linked infrastructure—Zodia Custody and Zodia Markets—is positioned as foundational to scaling prime services without starting from zero.

Payments infrastructure moved in the same direction: Visa added stablecoin payouts to Visa Direct through BVNK (announced Jan 14, 2026), enabling businesses to pre-fund stablecoin balances and push near-instant payouts to recipients’ wallets. Visa emphasized stablecoin wallets as an added endpoint alongside cards and bank accounts, and BVNK was cited as already processing $30B+ in annual stablecoin transactions, with prior backing from Visa’s venture arm and later Citigroup.

Attention liquidity dried up — and platform rules rewrote the game

On the distribution side, creators described a broad engagement drawdown across X and YouTube, with crypto content becoming harder to surface amid algorithm disputes, bot overload, and what was characterized as retail fatigue. The flashpoint included X’s head of product responding (in later-deleted posts) that feed mechanics are constrained—users see only ~20–30 posts per day on average—fueling creator frustration about reach and ranking. On YouTube, crypto viewership was described as at its lowest since early 2021, reinforcing the idea that the attention slump is multi-platform rather than a single-site glitch.

Then X hardened the line: apps rewarding users for posting would no longer be permitted API access (disclosed Jan 15), explicitly targeting systems blamed for spam and low-quality engagement. The immediate effect described was a repricing across InfoFi-linked social tokens—Kaito down about 20%, COOKIE down roughly 15%, and the InfoFi sector losing over 10% of an estimated ~$367M market cap—while projects began pivoting away from permissionless reward models toward tiered, more traditional marketing structures.

Onchain “plumbing” stayed active, but narratives got stress-tested

Onchain activity wasn’t uniformly soft. Polygon paired a major internal reset with a burst of network usage: Polygon Labs reportedly cut roughly 30% of staff as it integrated acquisitions valued at up to $250M and sharpened a payments-focused mission (“moving all money onchain,” per public statements cited). At the same time, January network fees topped $1.7M (strongest in ~14 months), attributed largely to Polymarket’s 15-minute markets, alongside ~5.3M daily transactions, ~1.4M active users, and 12.5M+ POL burned.

Elsewhere, the week showed how fast social narratives can outrun data. Solana’s official account took shots at Starknet with claims about usage, sparking backlash and replies from Starknet-linked accounts. In parallel, Starknet’s reported metrics improved: TVL climbed back above $300M (first time since early 2024) alongside higher stablecoin liquidity, and the same coverage pointed to STRK going live on Solana via NEAR Intents—putting an interoperability milestone next to the “war” discourse.

Execution tooling also drew capital, reinforcing the “infrastructure arms race” theme. YZI Labs disclosed a multi-eight-figure investment in Genius Trading (Jan 13, 2026) and confirmed CZ as an advisor. Genius positioned itself as a cross-chain trading terminal spanning spot, perpetuals, and copy trading across 10+ chains, citing $160M+ cumulative volume before its public debut and framing the product demand around better onchain execution as activity expands.

Flows flipped risk-on to selective — with macro expectations named as the driver

Positioning through investment products moved sharply: CoinShares data cited $454M in weekly outflows from crypto ETPs over four consecutive days, nearly erasing roughly $1.5B of inflows from the first two trading days of the year. The stated explanation was cooling expectations for near-term Fed rate cuts, tightening the link between crypto investment flows and macro pricing.

Even within those outflows, the flow map wasn’t uniform: Bitcoin and Ether products led withdrawals, while selected altcoin products (including XRP and Solana) still attracted inflows, and total ETP AUM was described as broadly stable.

Corporate balance sheets kept turning into crypto strategy vehicles

Treasury strategy stayed a headline driver. Strategy disclosed buying 13,627 BTC for about $1.25B after MSCI index inclusion, tying balance-sheet decisions to expanding passive institutional exposure. In the same window, Bitmine reported expanding ETH holdings to over 4.16M ETH, with combined crypto and cash reserves around $14B—presented as a distinct Ethereum-treasury approach relative to Bitcoin-only models.

Strive pushed further into corporate-Bitcoin territory: shareholders approved an all-stock acquisition of Semler Scientific that adds 5,048.1 BTC, taking combined holdings to ~12,800 BTC; shares fell roughly 12% after approval amid dilution concerns and a reverse stock split mentioned in the same coverage.

Not every “portfolio decision” leaned deeper into BTC. Jefferies strategist Christopher Wood removed Bitcoin from the Greed & Fear portfolio after holding it since late 2020, reallocating the prior 10% BTC sleeve into physical gold and gold-mining equities, citing quantum-computing risk as the core rationale and estimating potential exposure for about 30% of circulating BTC (as characterized).

Bitmine also broadened the idea of what an ETH-treasury company can do with capital: it said it intends to invest $200M into MrBeast’s Beast Industries (announced Jan 15; expected close on or about Jan 19), describing it as one of its largest deployments outside direct crypto holdings and framing the move as strategic rather than passive.

Top Weekly Altcoin Gainers and Losers

Gainers:

Dash DASH (+111.40%)

Chiliz CHZ (+38.98%)

Monero XMR (+36.69%)

Story IP (+33.91%)

Pump.fun PUMP (+27.94%)

Losers:

Polygon POL (-14.70%)

Virtuals Protocol VIRTUAL (-10.09%)

XDC Network XDC (-9.57%)

Litecoin LTC (-8.87%)

Bitcoin Cash BCH (-6.73%)

This article has been refined and enhanced by ChatGPT.